Setting up a proper bank account and financial structure is a vital step in launching and running a successful business. It helps separate personal and business finances, ensures legal compliance, improves financial tracking, and builds credibility with partners, clients, and investors.

This guide walks you through the importance of business banking, how to set up a business account, choosing the right bank, understanding financial tools, and tips for financial management.

1. Why Business Banking Matters

A dedicated business bank account offers numerous advantages

Separation of Finances

Keeps your business and personal expenses separate, which is essential for legal protection (especially for LLCs and corporations).

Improved Bookkeeping

Helps track income, expenses, and profitability accurately.

Professionalism

Makes your business look more credible to clients and vendors.

Tax Efficiency

Simplifies tax filing and audit processes.

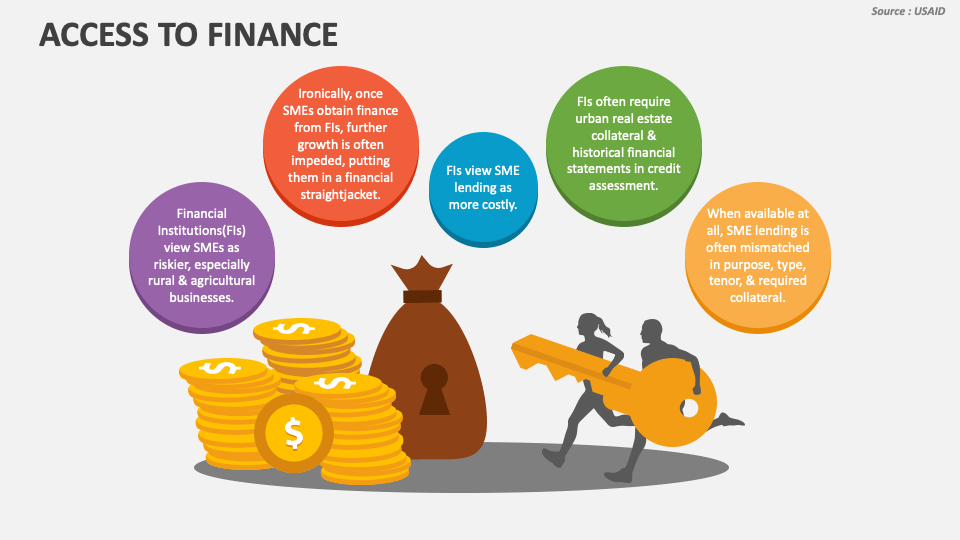

Access to Financing

Business accounts are often required to apply for loans or credit.

2. Types of Business Bank Accounts

There are several banking solutions available for businesses. The most common types include

Business Checking Account

Used for daily business operations like receiving payments and paying bills.

Comes with debit cards, checks, and online access.

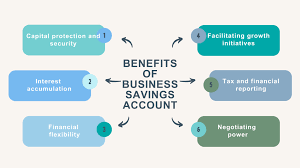

Business Savings Account

Helps businesses save for future expenses or taxes.

Earns interest on unused funds.

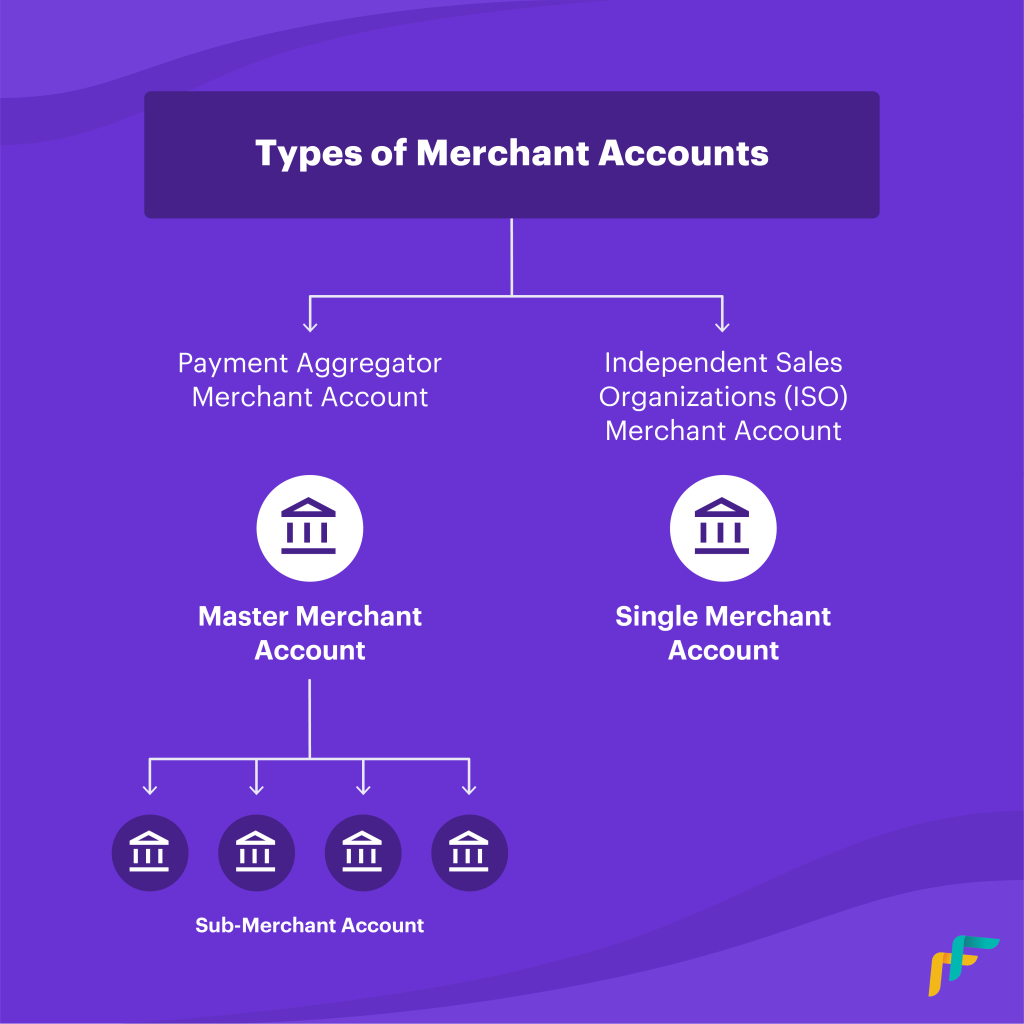

Merchant Account

Required if you plan to accept credit/debit card payments.

Works in conjunction with payment gateways or POS systems.

Business Credit Card

Useful for managing cash flow and building business credit history.

3. Documents Required to Open a Business Bank Account

Before heading to the bank, prepare the following documents:

Business Formation Documents: Articles of Incorporation or Organization.

EIN (Employer Identification Number): Issued by the IRS.

Operating Agreement or Partnership Agreement: If applicable.

Business License or Registration Certificate.

Valid Photo ID: For all account signers or business owners.

Banks may have specific additional requirements based on your business structure (LLC, corporation, sole proprietorship, etc.).

4. Choosing the Right Bank for Your Business

When selecting a banking partner, consider these factors:

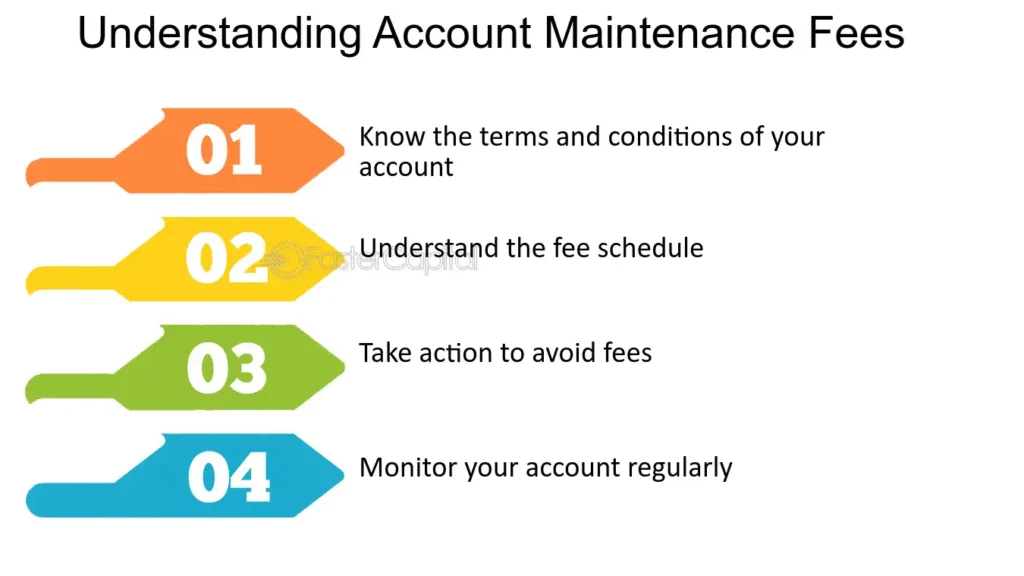

Fees

Check for monthly maintenance fees, minimum balance requirements, transaction limits, and ATM charges.

Accessibility

Is the bank conveniently located?

Does it offer robust online or mobile banking features?

Customer Service

Look for banks with strong customer support and business advisory services.

Integration

Can the account integrate with your accounting software or payroll provider?

Lending and Credit Services

Check if the bank provides access to business loans, lines of credit, or SBA financing

Recommended U.S. Banks for Businesses:

Chase Business Banking

Bank of America Small Business

Wells Fargo

Capital One Spark Business

Mercury (for online startups and tech companies)

Bluevine (online banking with high-yield interest)

5. Online-Only Business Bank Accounts

Online-only banks are growing in popularity due to lower fees and digital convenience. These banks cater especially well to e-commerce businesses and startups. Benefits include:

Quick online account setup.

No physical visits needed.

Easy integration with apps and payment platforms like Stripe, PayPal, or QuickBooks.

However, they may lack cash deposit facilities or in-person support.

Popular online business banks:

Mercury

Novo

Bluevine

Lili

6. Setting Up Accounting & Bookkeeping

Opening a business bank account is only the first step. You also need to set up systems for tracking and managing your money.

Choose Accounting Software

Popular accounting tools for small businesses:

QuickBooks

Xero

FreshBooks

Zoho Books

Wave (free)

These platforms help you:

Track income and expenses.

Generate profit & loss reports.

Automate invoicing and payments.

Prepare for tax filing.

Hire an Accountant or Bookkeeper

If your finances are complex or you’re unfamiliar with accounting, consider hiring an accountant. They can:

Ensure compliance with tax laws.

Help with payroll and sales tax.

Provide financial forecasting and advice.

7. Accessing Business Funding

After establishing your financial structure, you may seek funding to grow. Options include:

Business Loans: From banks or credit unions.

SBA Loans: Government-backed loans with favorable terms.

Lines of Credit: Flexible cash access when needed.

Venture Capital or Angel Investors

Crowdfunding: Through platforms like Kickstarter or Indiegogo.

Conclusion

Setting up a business bank account and organizing your finances is more than a formality—it’s the foundation of your company’s success. Whether you’re a freelancer, startup founder, or a small business owner, structured banking and financial systems make it easier to scale, stay compliant, and manage operations smoothly.

Invest time in selecting the right bank, keeping accurate records, and staying on top of cash flow. With the right setup and discipline, your business can thrive financially from day one.